First, let’s talk about funds. When a GP (e.g. a venture capital firm or private equity firm) has a certain investment mandate they need to satisfy, they will launch a fund and, in effect, pool capital to fulfill that directive.

Similar to how companies offer diverse products, firms will create distinct funds with different strategies to reach various markets or geographies. And often, if a fund is successful, the financial sponsor will launch another one that shares similar characteristics to the one that preceded it.

What is a fund family?

A series of funds that share the same strategy, geography and financial sponsor is what we call a fund family. Typically funds in a family will follow a similar naming convention (e.g. Fund II, Fund III and Fund IV), although there are some exceptions.

The idea of fund families, despite existing for a long time, has not had a widely accepted terminology within the private markets. At PitchBook, however, we have used this phrase for private market funds—and are coining it for use within the private markets.

Benefits of fund families

With fund families, investors are able to put capital toward a specific strategy with the same financial sponsor. Often, large firms will devote entire teams of personnel to a single strategy that may be focused on a geography or investment thesis. Not only is it convenient to track and build rapport with one firm, but a strong LP/GP relationship can have positive impacts on allocation efficiency and effectiveness. Additionally, in the eyes of both LPs and GPs, a fund family is a continuation of a successful investment thesis that is still worth devoting resources (both people and capital) to.

Given the similarities between funds in a fund family, it’s easier to compare performance. Understanding why one fund is outperforming another or how funds of the same strategy perform over time is important for finding high-performing vehicles. Especially within the private markets, it’s critical to benchmark investment opportunities against data that gives an apples-to-apples comparison, such as IRR, cash flow multiples or other metrics.

For example, PitchBook uses fund families to calculate step-ups and performance persistence. While past performance does not guarantee future results (as every investor has heard more than once), when it comes to investing in active managers, past performance is virtually always one of the first things considered. With a certain level of insight, LPs can better understand which firms have consistently shown returns and make an informed decision to work with them or not. At the same time, GPs can use fund performance to show success and attract more investors to their funds.

Examples of fund families

Fund types can vary widely—ranging from more standard venture capital funds to niche, specialized funds for private debt or secondaries, as you will see below.

Venture capital funds

Accel India Fund I – VI

Accel is a venture capital firm and lender based in Palo Alto, California. The firm has closed over 50 funds since it was founded in 1983, including six venture funds intended for investment in seed and early-stage investments in Indian startups.

Private equity funds

KKR Americas Fund I - XIII

Kohlberg Kravis Roberts is a global investment firm based in New York. The firm manages investments across multiple asset classes including private equity, real estate, credit strategies and hedge funds. In 2017, the firm closed its latest PE fund, KKR Americas XII Fund, at $13.9 billion intended for private equity-related transactions in the US, Canada and Mexico.

Niche or specialized funds

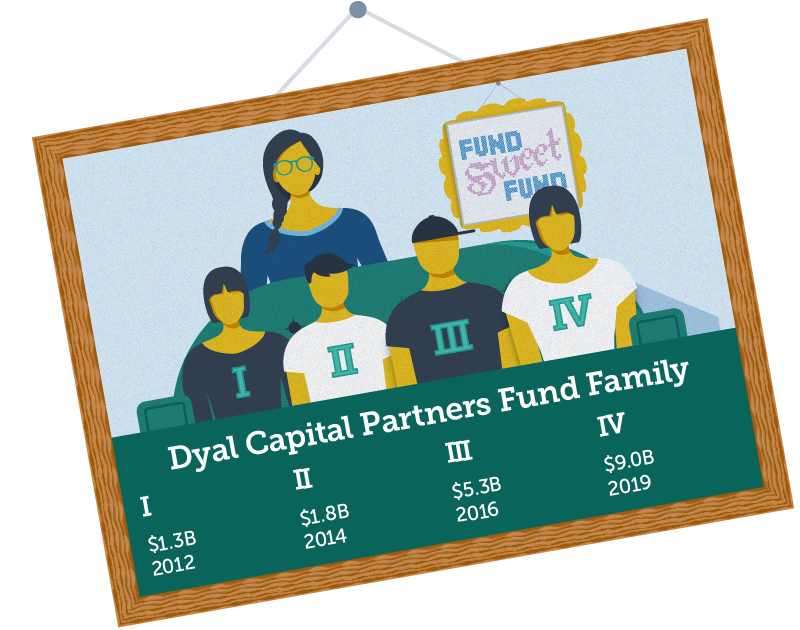

Dyal Capital Partners Fund I – IV

Dyal Capital Partners is a private equity investment firm based in New York. The firm recently closed its fourth growth fund in the Dyal Capital Partners Fund family at $9 billion and will use it to make GP stake investments, targeting deals between $500 million - $1 billion.

Private debt funds

Carlyle Strategic Partners Fund I – IV

The Carlyle Group is a private equity firm and business development company based in Washington D.C. In a series of private debt funds, Carlyle Strategic Partners Fund, the firm raised capital to invest in the debt and equity of operationally sound, but financially distressed companies.

Secondary funds

Hollyport Secondary Opportunities Fund I – VII

Hollyport Capital is a global private equity assets manager based in London. The firm acquires tail-end portfolios of mature interests in the secondary market and has launched seven secondary funds—all with highly diversified managers and geographies.

Confidently allocating capital to the right funds requires diligent evaluation of performance and strategy—especially amidst the proliferation of the private markets.

In early 2019, PitchBook conducted a survey of 101 institutional limited partners and public equity investment managers to better understand where the public and private markets intersect, including how investors look at allocation in today’s market.

Download the report, PitchBook Private Markets: A Decade of Growth, to see the results.