Since 2000, active private equity firms in the market have increased by 189 percent and PE-backed companies have shot up by 364 percent. In addition, VC and PE funds have a record $1 trillion in uncalled capital—due in large part to institutional investors’ increasing interest in the private markets. The increase in active firms, PE-backed companies and LPs involved in this space is contributing to (and is an indication of) the maturation of private equity. With greater competition, firms are jostling for LP commitments—and are pushed to develop unique specializations and competitive differentiators to help them stand out.

Specialization within buyout funds

As more investors vie for buyout targets, fund managers with unique skillsets and in-depth expertise are helping firms better compete and stand out to institutional investors. Instead of applying a generalist approach, many firms are opting to focus on solving specific challenges for portfolio companies. As an example, one fund manager may focus on taking companies from $5 million to $20 million in EBITDA in its domestic country, while another may focus on a company’s expansion into global markets.

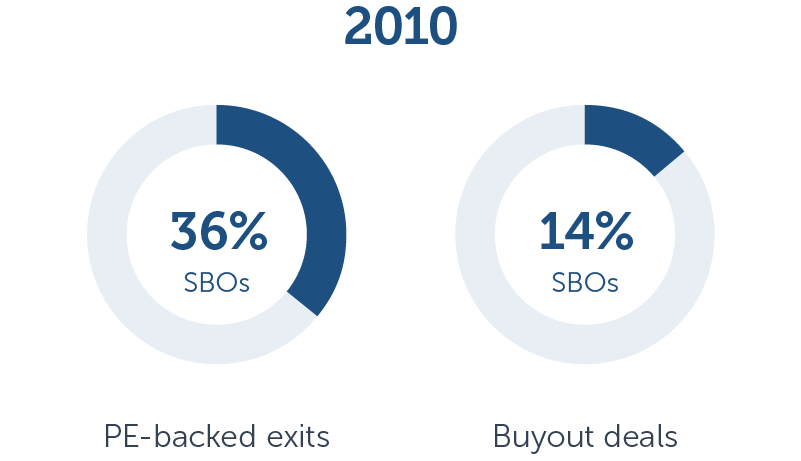

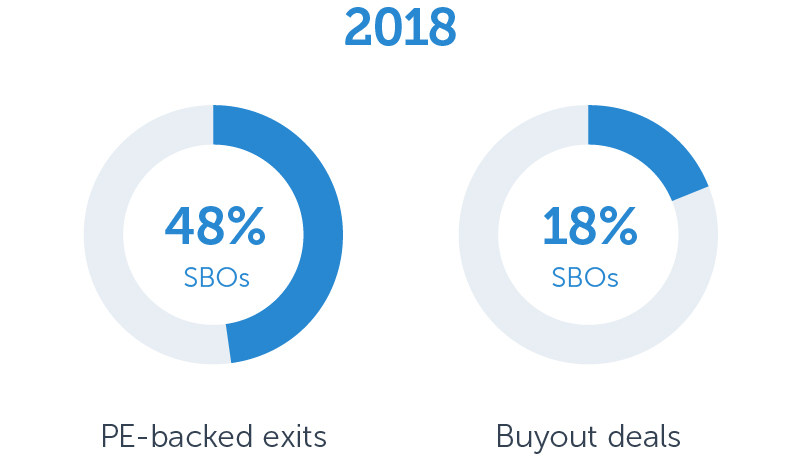

Additionally, an increase in PE-backed companies means many targets are already sponsored. This has caused PE investors—with record amounts of dry powder to deploy—to increasingly invest in less traditional targets like VC- and PE-backed companies, resulting in more SBO activity than ever. In 2010, secondary buyouts represented 36 percent of all PE-backed exits and were the source of 14 percent of all buyout transactions. Those percentages have since increased to 48 percent and 18 percent, respectively.

Source: PitchBook, data through 6/30/2018

Although these trends have developed separately, specialization lends itself well to executing secondary buyouts. Even if a portfolio company was previously PE-backed, a firm with a unique specialty can add value (and increase the company’s overall worth) through operational improvements or applying novel expertise. This is particularly important when so many targets already have backing.

Increasingly common niche strategies

Another way firms are adjusting to an ever-changing, competitive private market environment is through an increased focus on niche funds (those outside of traditional VC or PE, such as debt and GP stakes). Big names like Carlyle, which closed its $2.5B debt fund in early 2017, and Blackstone, with its long-running Strategic Partners secondaries series (including a $7.5B fund that also closed last year), have been expanding their businesses to include niche strategies. An even more recent shift involves funds targeting minority stakes in PE firms, as Goldman Sachs is doing through its Alternative Investments & Manager Selection Group.

A stronger investor appetite for private debt and secondaries funds—plus resilient fundraising—are combining to create higher demand for these niche funds. Coming from past perceptions of distress and underlying asset volatility, these strategies are now seen as prime opportunities to create alpha (especially given higher prices, risk and competition elsewhere in PE.)

Further, niche funds provide more ways for institutional investors to access private equity—addressing an increased desire for greater PE exposure. Not so long ago, the University of Texas/Texas A&M Investment Management Company (UTIMCO) increased its PE allocation from 17.5 percent to 25 percent—with ambitions to more heavily invest in niche areas of private equity. Niche funds can also help LPs diversify which regions, strategies, companies and vintage years they’re exposed to. For example, committing to just one secondaries fund exposes an LP to significantly more vintages than a commitment to a traditional buyout fund.

As the private markets continue to mature, PE firms will need to specialize to stay competitive. From hiring fund managers with specific expertise or opening niche funds—more and more firms will likely extend their business into new strategies and market themselves as one-stop shops for institutional investors.

See how various strategies, including private equity, secondaries and fund-of-funds, are performing with the latest PitchBook Benchmarks.