In 2018, larger funds, bigger deals and an increased appetite for alternative assets fueled a record-breaking total VC deal value of $131 billion—and an unprecedented flurry of unicorn activity. Last year saw a dramatic peak of unicorn deals with nontraditional VC participation, as this group contributed to $43.5 billion invested across just over 100 transactions. That activity continues today. So far in 2019, this cohort has participated in 53 unicorn financings totaling $17.7 billion. Impressively, 1H 2019 boasts a unicorn deal value that’s already higher than yearly totals for nontraditional investors chasing unicorns in 2016 and 2017.

What are nontraditional and tourist investors?

Looking at things from a higher level, nontraditional VCs and tourist investors include essentially everyone outside of traditional VC firms (such as corporations, LPs, PE firms, sovereign wealth funds, hedge funds, investment banks, etc.). This group is proliferating quickly, as more new participants become involved in venture capital.

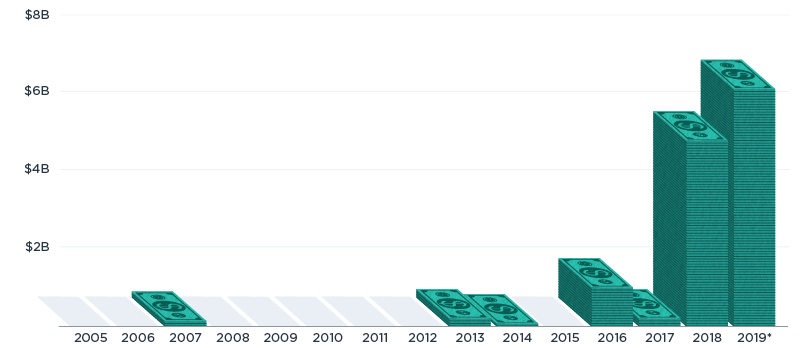

As investors from around the world are increasingly active in venture, they are fueling its ongoing globalization and the unicorn phenomenon. Last year, 12 unicorn-related deals with only foreign investor participation closed, worth a total of $4.8 billion. So far in 2019, even more capital has been introduced by this group, tallying over $6 billion in unicorn funding.

VC unicorn deal value with only foreign investor participation

So, why are these atypical VC investors looking to get more involved? In addition to the allure of unicorns, high prices all around—including management fees for traditional funds—have many firms looking into alternative ways to allocate capital to the private markets.

Secondary markets: venture capital’s increasingly popular liquidity release valve

Another major factor driving unicorn proliferation and encouraging participation from nontraditional VCs is a growing acceptance and usage of secondary markets to obtain liquidity. This path offers investors the opportunity to realize value and return capital without a full exit—something that is becoming increasingly critical as time to exit remains extended for unicorns (and other companies).

In some secondary transactions, foreign and nontraditional players are the buyers, whereas earlier investors are the sellers, but there’s no reason that process can’t repeat down the line—offering flexibility to those involved. It’s important to emphasize that multiple companies are now increasingly comfortable buying and selling the securities of large, privately held companies in private transactions at the scale of billions of dollars. Though this method may only really apply to a select number of companies, it’s likely to continue growing in popularity. Despite being considered by some as risky, these types of transactions have helped enable the continued existence of unicorns.

Though many factors have contributed to VC’s recent breakout year, part of this rise is due to nontraditional investors’ increasing willingness to spend more in the hopes of snagging a unicorn. These atypical investors have played a key role in the ongoing evolution of the unicorn phenomenon and the venture capital landscape—and you can expect this to continue for the near future.

To learn more about unicorns and the VC landscape, download the 2019 Unicorn Report.