Private equity (PE) and venture capital (VC) are two major subsets of a much larger, complex part of the financial landscape known as the private markets. Because the private markets control over a quarter of the US economy by amount of capital and 98% by number of companies, it’s important that anyone in any business capacity—from sales to operations—understands what they are and how they work.

In a previous article, we discussed the key differences between the public and private markets; namely, that companies within the public markets sell shares to the general population—who can then buy, sell, or trade them on a stock exchange—whereas companies within the private markets give professional investors equity in exchange for funding. Here, we’ll focus on the two largest markets that make up the private market landscape: PE and VC.

What are the similarities between PE and VC?

PE and VC firms both raise pools of capital from accredited investors known as limited partners (LPs), and they both do so in order to invest in privately owned companies. Their goals are the same: to increase the value of the businesses they invest in and then sell them—or their equity stake (aka ownership)—for a profit.

How are PE and VC different?

The main differences between private equity and venture capital

PE and VC primarily differ from each other in the following ways:

- The types of companies they invest in

- The levels of capital invested

- The amount of equity they obtain through their investments

- When they get involved during a company’s lifecycle

A closer look at PE vs. VC

Private equity investment firms often take a majority stake—50% ownership or more—in mature companies operating in traditional industries. PE firms usually invest in established businesses deteriorating because of operational inefficiencies. The assumption is that the companies could become profitable once those inefficiencies are corrected. This is changing slightly as PE firms increasingly buy out VC-backed tech companies.

By contrast, venture capital investment firms fund and mentor startups. These young, often tech-focused companies are growing rapidly, and VC firms provide funding in exchange for a minority stake of equity—less than 50% ownership—in those businesses.

How do PE and VC investors source funds?

While firms seek funding from various sources, they mainly rely on institutional investors, such as endowments, pension funds, insurance companies, and sovereign wealth funds. In addition to institutional investors, high-net-worth individuals (HNWIs) are a growing funding source for PE and VC firms. HNWIs are equally interested in growing their portfolios as traditional institutional investors and have increasingly invested in alternative investments such as private credit, digital assets, and real estate, providing more financial backing for companies.

Risk and return profiles of PE and VC investments

Private equity investing involves lower risk with a longer return horizon, whereas venture capital investments carry higher risk and the potential for higher returns.

In favor of nurturing the growth of startups and technological innovations, the venture space is characterized by higher risk. Companies in their infancy are still working on proof of concept and unestablished market positioning. However, they also carry a higher potential for disrupting industries and, therefore, achieving substantial growth.

Private equity places bets on long-term value creation and stability. These investors favor established, proven business models and cash flows over the long term.

Here, companies have already weathered market instabilities and the early stages of development and expansion. They have a proven concept that also states predictable returns. Firms drill into operational inefficiencies, and it’s also the place where they see the highest returns.

Ultimately, deciding to invest in venture capital or private equity-backed companies depends on your risk tolerance investment horizons and mandates.

How does private equity work?

PE investors also raise pools of capital from LPs to form a fund—also known as a private equity fund—and invest that capital into promising, privately owned companies. However, the companies PE firms want to invest in usually look different from the startups VC firms invest in.

To begin with, private equity investors might invest in a company that’s stagnant or potentially distressed but still has growth possibilities. Although the structure of private equity investments can vary, the most common deal type is a leveraged buyout (LBO).

What is a leveraged buyout?

In an LBO, an investor purchases a controlling stake in a company using a combination of equity and significant debt, which the company must eventually repay. In the interim, the investor works to improve profitability so that debt repayment is less of a financial burden for the company.

When a PE firm sells one of its portfolio companies to another company or investor, it usually makes a profit and distributes returns to the LPs that invested in its fund. Some private equity-backed companies may also go public.

Examples of PE-backed companies

- EQ Office: A Chicago-based owner and operator of office buildings in the US

- Panera Bread: A St. Louis-based owner, operator, and franchisor of retail bakery-cafes

- PetSmart: A Phoenix-based retailer of products and services for the lifetime needs of pets

- Toms Shoes: A Los Angeles-based manufacturer of shoes and footwear accessories

Examples of PE firms

- Kohlberg Kravis Roberts: A New York-based PE firm that invests in financial services, energy and business products

- The Carlyle Group: A Washington D.C.-based firm that targets commercial products, retail, and transportation

- The Blackstone Group: A New York-based firm invested in real estate, public debt, and secondary funds

- HarbourVest Partners: A Boston-based firm specializing in information technology, 3D printing and industrials

- Audax Group: A New York-based firm interested in software, media, and infrastructure

What factors do PE firms consider when assessing operational inefficiencies in mature companies?

Operational efficiency is influenced not only by streamlining processes but also by identifying inefficiencies. In established companies, where rapid growth may be limited, refining operations is a cornerstone of generating value for customers and investors.

When private equity firms look to improve operations, they consider aspects of due diligence informed by key performance indicators (KPIs). PE managers track progress by analyzing financial metrics, such as profit margins and cost structures, to spot areas where expenses might be disproportionate to industry norms. This often involves assessing product lines to phase out underperformers and rethinking capital management strategies such as the company’s debt-to-capital ratio.

The firm’s portfolio management team plays a vital role in overseeing the companies to ensure they stay on track with financial goals. These managers work closely with company leadership and proactively address risks before they grow into larger issues.

Another consideration is technology integration; outdated systems and a lack of automation can lead to major operational hurdles. In today’s landscape, using technology solutions to streamline processes is essential. With advancements in AI and ML, staying competitive requires embracing new technologies quickly and consistently.

How do investors measure operational efficiencies?

A commonly used metric for PE investors assessing operational efficiency is the cost-to-revenue ratio, which calculates the total expenses involved in producing a product compared to its revenue. A lower ratio means the company spends less to create its offerings. Productivity measures like revenue-per-employee also help companies compare their performance with competitors and gauge their position in the market.

How does venture capital work?

To raise the money needed to invest in companies, VC firms open a fund and ask for commitments from LPs. Using this process, they draw from the money they invest into promising private companies with high growth potential. As companies grow, they go through different stages of the venture capital ecosystem. VC firms usually focus on one or two VC funding stages, which impacts how they invest.

If a company a VC firm has invested in is successfully acquired or goes public through the IPO process, the firm makes a profit and distributes returns to the LPs that invested in its fund. The firm could also make a profit by selling some of its shares to another investor on what’s called the secondary market.

Examples of VC-backed companies

- Juul: A San Francisco-based manufacturer of e-cigarettes and nicotine products

- Stripe: An online payments processing platform headquartered in San Francisco

- SpaceX: A Los Angeles County-based designer and manufacturer of rockets and spacecraft

- Waymo: A developer of a self-driving technology in the Bay Area

- Ripple Labs: A developer of a blockchain platform headquartered in San Francisco

Examples of VC firms

- Accel: A Palo Alto-based VC firm that targets SaaS, fintech, and information technology companies in their early stages

- Benchmark: A San Francisco-based firm invested in consumer services, communication, and software

- Madrona Venture Group: A Seattle-based firm that invests in e-commerce, gaming, and digital media

- Sequoia Capital: A Menlo Park-based firm interested in fields such as nanotechnology, financial services, and healthcare

- Venrock: A firm based in Palo Alto, CA, which specializes in tech, software, and cloud services

How do VC firms determine which startups have the highest growth potential?

The venture capital valuation process determines whether a startup is a worthwhile investment. During their due diligence phase, VC firms dig deep into research and verify their assumptions to arrive at accurate valuations. While various methods exist, the Venture Capital Method and the Burkas Method are among the most common.

The Venture Capital Method focuses on figuring out how much a startup is worth before and after an investment. This is often calculated through pre-money and post-money valuations—a method ideal for startups experiencing significant growth and planning to exit soon.

A pre-money valuation is the value of a startup before it receives investment—estimating how much equity an investor will get in exchange for their capital. On the other hand, a post-money valuation is the startup’s value after an investment.

These methods are also used to help the VC firm calculate the ownership percentage of new and existing investors. They use a company capitalization table, or cap table, to view ownership stakes and the company’s equity value. It provides a holistic picture of who owns what percentage of each company.

The Burkas Method assesses qualitative factors and examines a startup company’s operational efficiency and risks. It is ideal for an early-stage or pre-stage startup and is widely used in tech.

VC firms assess startups through a combination of qualitative and quantitative approaches. Other important factors they assess include market size estimates, revenue generation, the founding team’s experience, risks, and exit opportunities in the addressable market.

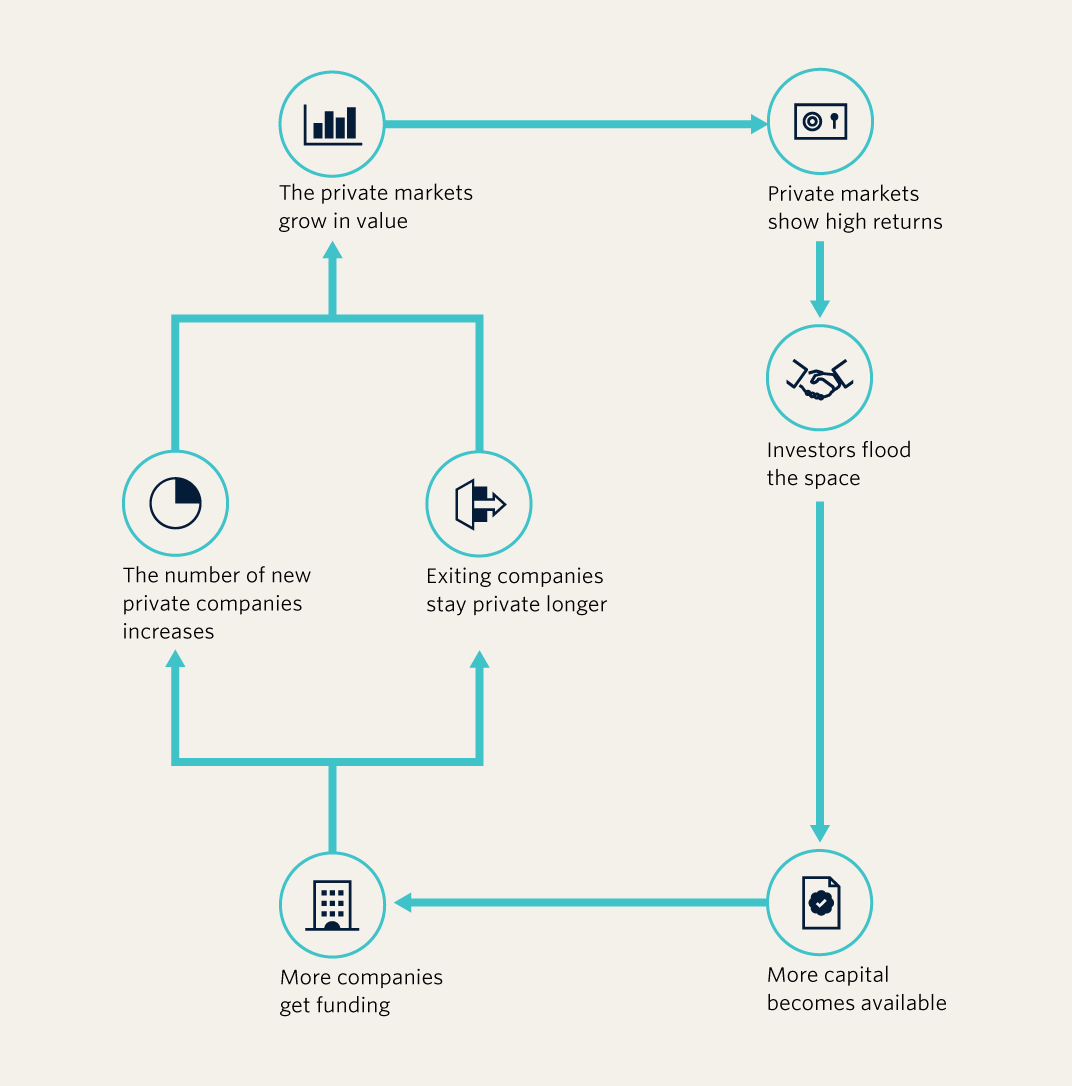

Why are the private markets becoming more valuable?

Increased private market fundraising over the past three decades highlights the significant role VC and PE play in shaping businesses in all stages of development. These firms have contributed to the development of innovative technologies, the growth of established enterprises, and funding companies in distress.

In the past, companies often went public when their need for capital exceeded what investors could provide. With a public debut, a company could quickly raise a large sum of money from public shareholders and use it to scale. However, with market volatility and ongoing liquidity concerns in 2023, that approach has changed.

Navigating private market changes

The VC and PE landscapes have undergone significant shifts following broader market volatility, which increased regulations and changed investor sentiment. As a result, risk-averse limited partners (LPs) who funnel large volumes of capital into the markets have prioritized due diligence and risk assessment to a much greater extent. This has put added pressure on startups because general partners (GPs) seek to invest in companies with resilient business models.

In private equity, the emphasis is on value creation, and strategic optimization of portfolio companies has taken center stage. Investors try to find relief from the denominator effect, prompting an alternative means of rebalancing portfolios and generating inorganic growth as valuations fluctuate. With GPs (e.g. VC and PE firms) holding on to assets for longer, LPs received fewer fund distributions, and both players have turned to alternative means of maintaining liquidity. This also meant increased allocations in alternative and private market assets, with private debt being a preferred choice.

Q3 2023 Global Private Debt Report

To learn more about which strategies are thriving and which are out of favor in today’s environment, read our Q3 2024 Global Private Market Fundraising Report.

How do PE and VC work together?

As capital flows through the private markets, it moves from entity to entity through a series of financial transactions. Every time capital changes hands in the private markets, professionals advise on or execute the transaction, which then initiates a growth or transition phase for the company or companies involved. The map below illustrates a simplified version of these exchanges.

How PE and VC firms are growing through secondaries

Ongoing market volatility has prompted investors to seek alternative paths to prop up portfolio company growth. In a stalled exit landscape, firms are maintaining access to liquidity by investing their fund’s interest in a more mature portfolio.

Also known as continuation funds, secondary investments purchase existing assets from a primary fund or LP and sell that interest to a secondary buyer. They allow investors to avoid selling in an unfavorable market while the buyer benefits from faster returns.

These continuation vehicles are increasing in popularity and are utilized by general partners (GPs) in VC and PE firms to provide alternative exit opportunities for their investors. As the market evolves, secondary investments will continue to offer new paths to value creation, redistribution, and portfolio optimization.

Q4 2024 PitchBook Analyst Note: GP-Led Secondaries

GP-Led secondaries continued to flourish in 2024 driven by increased investment in continuation funds. Learn more in our Q4 2024 PitchBook Analyst Note: GP-Led Secondaries.

Maximizing returns through strategic add-on investing

In today’s uncertain market, add-on investments have become the go-to strategy for PE financing. With risk-averse syndicated loans on pause, investors are turning to smaller acquisitions to keep their portfolio companies afloat. These add-on deals have become the core of PE financing, helping investors weather the denominator effect and create inorganic growth through EBITDA.

An add-on investment is a strategy in which an investor purchases a smaller company at a lower valuation and merges it with one of its existing portfolio companies. The acquisition helps to expand its multiples and accelerate inorganic growth and competitive position. In selecting a complementary business, investors are creating more resilient entities better equipped to deal with market shifts.

More about the private markets

Explore the features that make PitchBook an essential resource for private equity and venture capital

Check out our robust private equity data

Check out our comprehensive VC data

From accelerator to zombie fund—the private market terms you need to know

Discover our VC, PE and M&A glossary

Explore the fast-growing and evolving private markets

Download our guide to understanding the private markets